Central Banks Deal A Helping Hand

Stock markets rallied in September as central banks across the globe are easing monetary policy despite an environment that lacks the traditional triggers for these cuts. The TSX led the way on the back of a strong commodity environment, rising 3.8%. The MSCI All Country World Index followed, up 2.8% while the S&P 500 rounded things out, up 2.7%. Interestingly, equity strength continues to broaden in the U.S. as the equal-weight S&P 500 (RSP) rose 4.2%. This demonstrates less reliance on the big cap tech names to carry the load.

Within the commodity complex, Copper fed off a large policy turn in China to rise 7.3%, leading the Bloomberg Commodity Index to a 4.4% monthly return. Gold continued its outperformance, rising 4.9% as market participants include the impact of loose global policy in their value estimates. Interestingly, WTI crude oil remains an outlier, falling 5.2% in September. Energy prices have certainly weakened due to increased supply announcements out of the middle east. However, a reversal could originate from the extended sell off in the U.S. Dollar. We also note that energy speculators keep reducing exposure, which sets up for a turnaround, but undoubtedly a technical price confirmation is needed to be more constructive.

Investors came into September increasingly optimistic that U.S. Federal Reserve Chairman Jerome Powell would cut rates 50bps instead of the initially priced 25bps. Powell did not disappoint on 18-Sep-24 as he slashed the target policy rate 50bps to 4.75%-5.00%. He also continued to emphasize the committee’s laser focus on the jobs market as a basis for future rate reductions. The Fed now sees the year-end policy rate at 4.38% which paves the path for some additional easing measures in the coming months. Equities initially popped over 1% following the announcement, but quickly lost their momentum to end the day down slightly. However, this was mostly an issue of positioning. Overall, the trend has been positive since the announcement and supported by the falling U.S. Dollar Index (DXY), which slipped 0.4%. Remarkably, the dovish Fed announcement marked a bottom for the long end of U.S. Treasury yields. The 10-year and 30-year yields flattened at 3.63% and 3.94%, before rising to 3.73% and 4.07%, respectively. With the Fed easing ahead of any material slowdown in the economy, markets may be starting to sniff out a rebound in economic growth and in turn inflation. Attention needs to be focused on the USD to confirm this as a bottom would have far reaching impacts across markets.

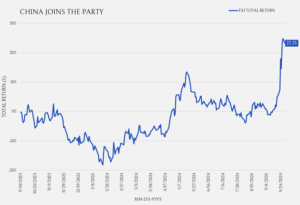

The Fed’s loose stance took some by surprise, but it was nothing relative to the reaction from China’s stimulus. China’s announcement was a full-180 from policymakers who had previously refrained from opening their purse strings. Demographic headwinds, a slowdown in the real estate sector, the re-emergence of state-led economic policymaking and COVID obstructions conspired to stall growth for several years, On 24-Sep-24, the People’s Bank of China (PBOC) announced its biggest inducements since the pandemic. These incentives include lowering short-term interest rates, providing funding programs to facilitate stock purchases and buybacks and allowing state-owned firms to buy unsold property by borrowing up to 100% from the central bank. A second declaration later in the week involved the issuance of CNY 2Tr (US$ 284Bn) in special sovereign bonds to support household consumption and to clean-up local government debt. On top of that, President Xi and the Politburo plan to announce a fiscal policy update on 03-Oct-24. The combination of monetary and fiscal stimulus was well-timed, after the U.S. rate cut, to limit the downside impact on the Renminbi. The Chinese government has maintained relatively low debt levels and has over USD 3Tr in foreign exchange reserves. Chinese stocks re-rated aggressively following the announcement. The iShares China Large Cap Index (FXI) was scraping a 0% year-to-date return as of 12-Sep-24, but printed a gain for 2024 of 23.3% at month-end.

Monthly Market Recaps