Market Reacts to Recession And Tariff Fears

One month ago, we discussed the Trump administration’s tariff announcements and their initial impact on currency markets. Since then, stock markets initially rallied to all-time highs on 19-Feb-25 but have subsequently retreated amid continued uncertainty around tariff policies. The US stock market has fallen approximately 9% from its February peak at the time of writing.

Interestingly, these US-announced tariffs have primarily acted as a self-inflicted wound on US markets, with Canadian stocks experiencing only half downside losses as US stocks, while International stocks (measured in USD) have remained resilient. Meanwhile, fixed income has served as an excellent portfolio stabilizer during this period—providing a welcome contrast to the 2022 high-inflation environment that negatively affected both stocks and bonds simultaneously. And lastly, the Alternatives sleeve of your portfolio has tempered this downturn, an area which we have proactively looked to enhance and expand over recent years which can play an important role in dampening portfolio volatility and in some cases capitalizing on downwards trends in markets.

Tariff Policy Uncertainties and Stagflation Concerns

Considerable ambiguity remains regarding which additional tariffs will be implemented in early April, which countries and sectors they will target, and their expected duration. The Trump administration has characterized this as an adjustment period citing “short-term pain for longer-term gain.” There are potential benefits if government deficit levels decrease, agencies operate more efficiently, and critical industries develop stronger domestic redundancies.

However, a significant risk emerging from the current policy trajectory is the potential for stagflation—a challenging economic environment characterized by slowing growth combined with persistent inflation. Tariffs typically increase consumer prices while potentially constraining economic activity, creating conditions that can lead to stagflationary pressures. The last significant period of stagflation in the 1970s proved particularly difficult for investors.

Economic theory and historical precedent have consistently demonstrated that trade barriers typically create more economic harm than benefit for the implementing nation. The current market reaction reflects investors’ recognition of these fundamental economic principles. The resulting volatility represents the market’s attempt to price in both the direct impacts of higher consumer costs and the indirect effects of supply chain disruptions, retaliatory measures from trading partners, and the overall chilling effect on business investment.

Cross-Border Economic Implications

While Canada has thus far weathered the market volatility better than the US, this may not persist if tariffs become a long-term fixture of North American trade policy. Canada’s economy is deeply integrated with and heavily dependent on US trade, with approximately 75% of Canadian exports destined for the US market. If substantial tariffs remain in place for an extended period, the Canadian economy faces a heightened risk of recession. A potential recession in Canada would likely have spillover effects for US companies with significant Canadian operations or customer bases, creating a negative feedback loop that could further dampen North American economic growth broadly.

Manufacturing adaptations, such as establishing new automotive factories, require significant time and could lead to supply chain disruptions that further fuel inflationary pressures while economic growth stalls. Additionally, the undermining of previously established trade frameworks like the USMCA creates business uncertainty that could hamper investment and growth, potentially exacerbating stagflationary tendencies across North America.

Potential Catalysts for Market Recovery

With those risks mentioned above in mind, there remain several factors which could drive a meaningful market rebound in the coming weeks/months:

1. Policy Clarity: Greater certainty around tariff implementation—or potential rollbacks of previously announced tariffs—would provide businesses with a more stable operating environment.

2. Fiscal Stimulus: Congressional action on individual or corporate tax reductions, though potentially problematic for deficit levels, could boost corporate profitability.

3. Technological Innovation: Continued R&D from major technology companies could yield productivity improvements as AI and other advancements mature and become further integrated into everyday business operations.

The Importance of Long-Term Perspective

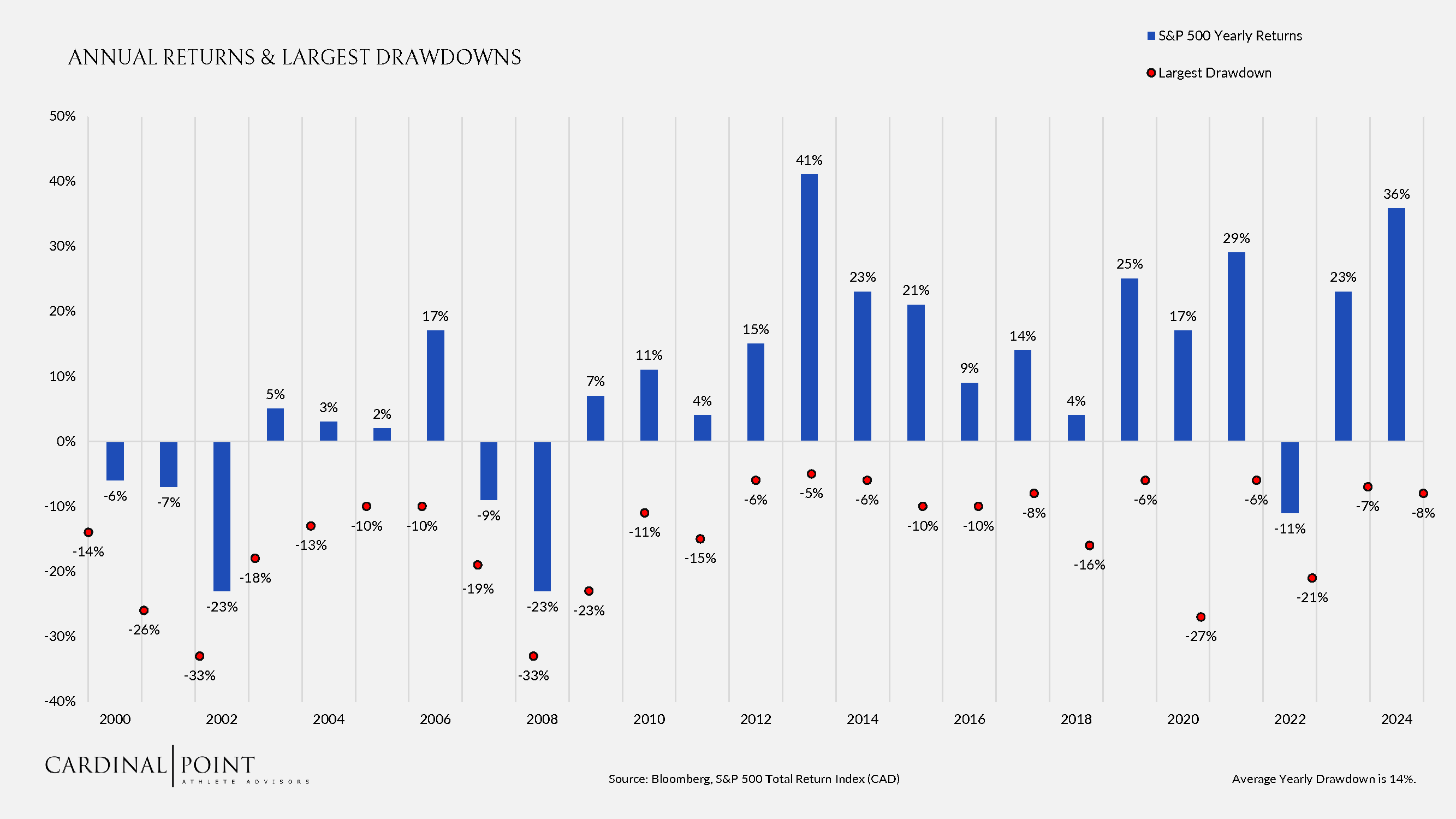

While we anticipate continued short-term volatility, it’s worth noting that most clients remain approximately flat performance wise for the early year to date period, following two consecutive years of exceptional growth in 2023 and 2024. The chart below clearly demonstrates that despite routine and significant pullbacks, equity markets have historically rewarded patient investors.

• Market Corrections Are Normal: The 14% average intra-year decline shown in the chart underscores that the current pullback is well within normal expectations.

• Diversification Benefits Emerge: International equities, fixed income, and defensive alternatives—which may have underperformed in recent years—often assume greater importance during market rotations.

• Time Horizon Matters: Looking beyond short-term fluctuations to 3-, 5-, and 10-year horizons consistently reveals positive expected returns for stocks.

Strategic Considerations for Long-Term Investors

As we navigate this period of uncertainty, several principles remain essential for long-term investment success:

• Asset Allocation Discipline: Maintaining appropriate diversification across asset classes helps manage volatility while positioning portfolios for long-term growth.

• Rebalancing Opportunities: Market corrections often present opportunities to rebalance portfolios at favorable valuations.

• Tax-Loss Harvesting: Current market conditions may present opportunities to harvest losses for tax efficiency which we will review.

Conclusion

It remains uncertain whether this “tariff tantrum” will be a traditional 5-15% short-lived correction or a more prolonged period of stagflationary challenges. As the historical data demonstrates, even years with significant intra-year drawdowns frequently finish with positive returns. This environment may or may not mirror the relatively quick recoveries we saw in 2020 and 2022, but our long-term outlook remains constructive while acknowledging these risks. The current volatility underscores the importance of diversification and patience in achieving investment objectives.

As always, we remain committed to monitoring market conditions and proactively managing portfolios to align with long-term investment objectives. If you have any questions or would like to discuss your portfolio in more detail, please don’t hesitate to reach out to your portfolio manager.

Indexes are unmanaged baskets of securities that are not available for direct investment by investors. Index performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Foreign securities involve additional risks, including foreign currency changes, political risks, foreign taxes, and different methods of accounting and financial reporting. Emerging markets involve additional risks, including, but not limited to, currency fluctuation, political instability, foreign taxes, and different methods of accounting and financial reporting. All investments involve risk, including the loss of principal and cannot be guaranteed against loss by a bank, custodian, or any other financial institution. Portfolio management and investment advisory services are provided by our affiliate, Cardinal Point Wealth Management.

Investment Management